The bull run in the housing market continues as residential realty remained buoyant with surging new supply and sales. Both end-users and investors are driving the residential market with an end-user -investor ratio of 71: 29. As many as 52% investors are millennials.

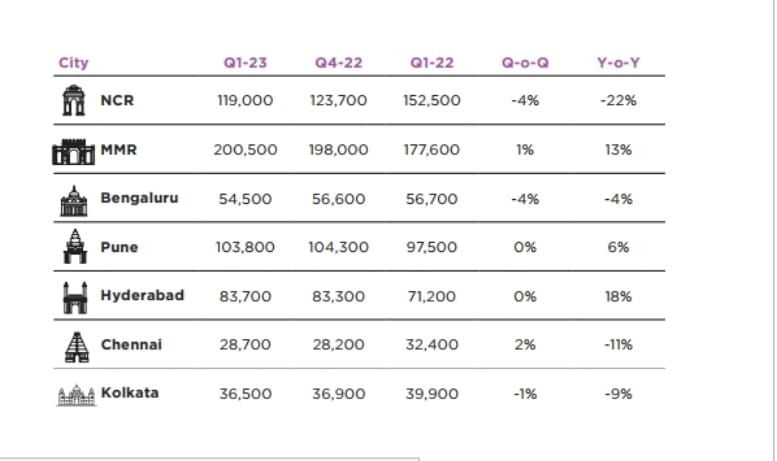

According to a recent CII-Anarock report, quarterly housing sales (Q1 2023) reached an all time high with nearly 113770 units sold across top 7 cities. Among the top cities, MMR and Pune accounted for over 48% of total sales with Pune registering a 42% yearly jump. The consumer sentiment for bigger homes continues unabated with 42% preferring 3BHK units. As many as 40% home seekers prefer 2BHK units , 12% opt for 1BHK units and 6% prefer homes exceeding 3 BHK units. At least 36% home seekers prefer a home that will be ready within a year.

New launches breached the 1 lakh mark , witnessing 23% yearly rise to 109570 units. The surge in new supply can be attributed to the unwavering appetite for homeownership. Mid-segment homes priced Rs 40-80 lakh continue to dominate new supply with 36% share followed by the premium segment(Rs 80 lakh-Rs 1.5 crore) share of 24% and affordable segment (less than Rs 40 lakh) share of 18%. MMR and Pune account for 52% of total new launches, recording 58% and 34% yearly increase in new launches respectively.

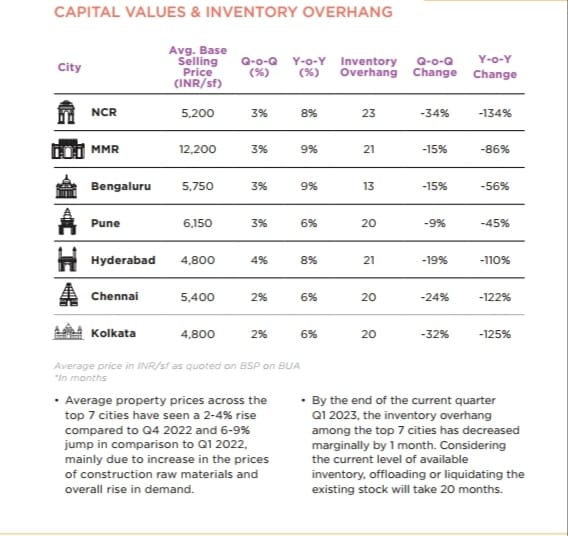

Despite substantial rise in new launches , available inventory in top 7 cities has not risen and remained similar at 6.27 lakh in Q1 2023, to inventory in the earlier quarter. On a QoQ basis unsold stock saw 1% dip with NCR seeing a highest decline of 22%.Inventory overhang declined to 20 months by end Q12023, compared to 27 months by end Q1 2022,, registering a YoY decline by 7 months. Bengaluru has the least inventory overhang of 13 months while NCR has a highest overhang of 23 months. Since inventory overhang of 18-22 months is considered healthy, the housing market is riding high on a positive sentiment.

1

2

3

4

5

6