Supported by a resilient economy and driven by buoyant consumer sentiment, robust property launches, competitive pricing and a conducive interest regime, residential realty has charted a high growth path, registering the highest housing sales during the first half of 2023.

Maintaining its growth momentum, the residential market has continued its upward trajectory in the first six months of 2023, clocking 15-year high home sales of 126500 units, recording a 21% YoY increase.

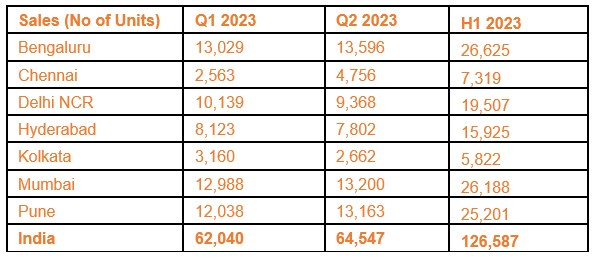

The strength of the residential market is evident from the robust sales volume recorded in the first half of 2023, with more than 62,000 units sold in each of the two quarters. Notably, Q2 2023 saw sales of over 64,500 units, representing a significant 4.0% quarter-on-quarter growth. It is interesting to observe that residential sales have consistently reached new peaks in each successive quarter over the past year. Aligning with this trend, Q2 2023 surpassed the previous historic high achieved in Q1 2023, making it the highest quarterly sales since 2008.

Prominent national and regional developers have experienced a substantial increase in sales for their new launches, driven by a strong interest from home buyers. Upon examining the quarterly reports of reputable developers, it is evident that 2023 is poised to establish itself as another record-breaking period for the residential market. This determination is based on the robust supply pipeline that developers have planned for the second half of the year, supported by sustained demand fundamentals.

H1 2023 Housing Sales

Note: Mumbai includes Mumbai city, Mumbai suburbs, Thane city, and Navi Mumbai. Data includes only apartments. Rowhouses, villas, and plotted developments are excluded from this analysis. Source: Real Estate Intelligence Service (REIS), JLL Research

Citiy-Wise Share in Total Housing Sales

Note: Mumbai includes Mumbai city, Mumbai suburbs, Thane city, and Navi Mumbai. Data includes only apartments. Rowhouses, villas, and plotted developments are excluded from this analysis. Source: Real Estate Intelligence Service (REIS), JLL Research

The larger markets of Mumbai and Bengaluru led the half-yearly sales, contributing 21% each of the total. Pune too made substantial strides accounting for 20%. In fact, all cities except Kolkata saw sales rise in H1 2023 compared to the year-ago period.

“The government’s strong push, coupled with the Reserve Bank of India’s decision to pause the repo rate in the last two instances, along with moderate inflation, have played a pivotal role in revitalizing the residential market. The demand for homes is projected to reach a new high in the second half of the year due to upcoming festive season and positive customer sentiment. The alignment of residential demand and supply is expected to pave the way for sustained growth in this segment.” says Siva Krishnan, Senior Managing Director and Head – Residential, India, JLL.

New Launches Lead the Sales Momentum

It is interesting to note that in H1 2023 the majority of the residential sales was driven by projects launched in the last 18-month period. According to Dr. Samantak Das, Chief Economist and Head Research & REIS, India, JLL, interestingly, around 58% of the sales recorded in H1 2023 (73,000 units) were contributed by projects that were launched from January 2022-June 2023. The increased traction in demand for recently launched projects depicts the increasing consumer confidence in under-construction projects as well. Over the last few years, there has been a robust influx of supply by branded developers. On the back of quality products, that are well-executed and getting delivered within the stipulated timelines, the risk appetite for consumers is also increasing.”.

It is also pertinent to note that older inventory, which was launched before 2018 and is nearing completion is also seeing traction. Developers are focusing on the timely completion of these on-going projects, leading to an increased interest in them. In H1 2023, around 12% of the sales were contributed by projects that were launched before 2018.

Notably, recent property launches have targeted not only the mid-segment but also the premium segment. Developers have become more cognizant of consumer demand in the post-COVID era and are aligning their launches accordingly, resulting in increased traction. These developers are launching premium residential projects and larger, well-amenitised plotted developments with integrated support infrastructure.

With unsold inventory declining in quality projects and limited ready-to-move options, completed projects constributed to only 13% of the half-yearly sales in 2023.

Mid & Premium Segments Drive Housing Sales

The mid-segment apartment projects (INR 50 lakh – INR 75 lakh price category) dominated the half-yearly sales with a 24% share. However, the premium segment (more than INR 1.5 crore) also had a substantial share of around 21% in the H1 2023 sales volume.

The share of affordable apartments priced below INR 50 lakh declined from 24% in H1 2022 to 19% in H1 2023 sales. A similar trend was witnessed in mid-segment apartments where the share, though still the highest, has seen a drop from 28% in H1 2022 to 24% in the current first half.

The proportion by which sales are increasing in the premium segment (priced above INR 1.5 crore) is significantly higher compared to that of mid-segment apartments. Sales grew by 37% y-o-y in the case of premium apartments in H1 2023 whereas it increased by just 4% in the mid-segment. As a result, the share of premium apartments in half-yearly sales increased from 18% in H1 2022 to 21% in H1 2023. Apartments in the price category of INR 1 crore- INR 1.5 crore have seen the highest growth in sales of around 67% y-o-y in H1 2023. Their share has also increased from 14% in H1 2022 to 19% in H1 2023.

Segment -Wise Sales Share

Source: Real Estate Intelligence Service (REIS), JLL Research

Robust demand leads to rise in capital values across the top 7 cities in India

Residential prices in major cities have risen in the range of 6-9% y-o-y, though Bengaluru has witnessed the highest increase of around 11-12% y-o-y. Kolkata, with an improving buyer sentiment, has started seeing a positive movement in prices as well, albeit at a slower pace, with prices up by 2% y-o-y. The rise in prices is seen across the spectrum of new projects that are seeing strong buyer demand. Even new phases of existing housing projects are being launched at higher prices. Despite the increase in prices, the sales traction remains very robust.

In the first quarter of 2023, an additional 14,000 units were sold in the plotted developments and villa categories in the top seven cities. Most of the sales activity was concentrated in the southern cities of Bengaluru, Chennai, and Hyderabad.

New launches remained buoyant in H1 2023

Residential launches of more than 151,000 units were recorded in H1 2023, a rise of 24% y-o-y. The launches also increased on a quarterly basis with over 76,000 units launched in Q2 2023. Encouraged by a strong consumer demand, developers have launched projects across the top seven cities of India. Most of the new launches were witnessed in Mumbai (24%), Pune (22%), and Hyderabad (19%).

City-Wise New Launches

Notably, the majority of the new launches in H1 2023, were in the premium segment (apartments in the price bracket of above INR 1.50 crore) with a share of 29%. Around 24% of the launches were in the price bracket between INR 1 crore- 1.5 crore.

As of Q2 2023, unsold inventory across the top seven cities of India increased by 2% on a q-o-q basis with new launches outpacing sales. Mumbai, Hyderabad, and Bengaluru together accounted for 63% of the unsold stock. An assessment of years to sell (YTS*) shows that the expected time to liquidate the stock has declined from 2.7 years in Q1 2023 to 2.5 years in Q2 2023, indicating robust sales growth.

Outlook:

India has succeeded in sustaining economic growth and maintaining job stability, resulting in phenomenal growth for the residential market over the past year. With policy rates unchanged in the last two monetary policy meetings by the RBI, potential homebuyers can continue to access housing loans at existing interest rates, thereby boosting the demand for residential properties.

In H2 2023, steady launches are anticipated as developers expand their land banks, capitalizing on expected interest rate moderation, growing housing demand, and support from institutional funding agencies. Reputed developers have announced a robust supply pipeline, through new launches within the next 7-8 months.

Driven by unprecedented sales, new residential projects are expected to gain further strength through strategic land acquisitions in key locations and growth corridors. JLL analysis reveals that the majority of land deals in the past year were made for proposed residential developments. Out of the total 2,181 acres of land transacted between January 2022 and May 2023, approximately 84% (around 1,822 acres) is allocated for proposed residential developments.

Notably, some of the prominent regional developers are expanding into new markets to tap into the growing demand in the top 7 cities. As a result, the outlook for 2023 is bright, with steady growth expected in the mid-segment as well as the premium and luxury segments.

1

2

3

4

5

6