While foreign institutional investments into real estate have started on a positive note, domestic investments are also gaining ground, presenting positive prospects for investments in the real estate sector.

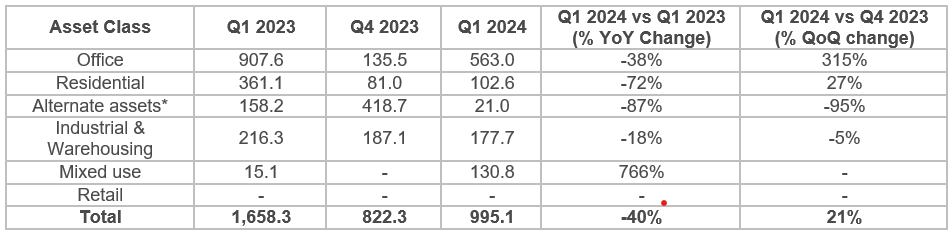

Institutional investments in the Indian real estate sector touched USD 1.0 billion in the first quarter of 2024, signaling a steady and positive start to the year. While this was a 40 percent drop compared to the same period last year, India’s real estate investments showed improvement on a sequential basis registering 21 percent QoQ rise. Foreign investments retained their dominance, forming 55 percent of the total inflows during the quarter. Domestic investments too witnessed a notable rise at 15% YoY in Q1 2024. The share of domestic inflows in overall institutional investments continued to rise to 45 percent in Q1 2024, compared to 24 percent in Q1 2023. Apart from the core asset classes such as office, institutional investments in industrial & warehousing and residential segments were noteworthy in the first quarter. The segments received capital inflows to the tune of USD 0.2 billion and USD 0.1 billion respectively in Q1 2024, forming a combined 28 percent of the total investments.

“At USD 1 billion, institutional investments into Indian real estate have started on a steady positive note. Interestingly, domestic investors are increasingly gaining more ground in Indian real estate. It is evident in the whopping 45 percent share in Q1 2024 investments, a marked surge from prior years. Within domestic institutional investments, office and residential assets formed about 66 percent, reflecting a strategic approach to align with India’s growth trends. This also underscores growing confidence of diversified spectrum of investors across multiple investment strategies including credit and acquisitions,” said Piyush Gupta , Managing Director, Capital Markets & Investment Services at Colliers India.

Office and Industrial Realty Driving Investment Inflows

At USD 0.6 billion, office sector accounted for 57 percent of the total investment inflows during Q1 2024. Foreign investments remained predominant, driving over two-thirds of the sector’s inflows, reinforcing the confidence of global funds in the fundamentals of commercial office real estate in India. Institutional investors continued their preference for completed and pre-leased income-yielding office assets as compared to greenfield developments. With a collective 81 percent share, Bengaluru and Hyderabad were the leading markets for office investments, mirroring the robust office demand seen in these cities this quarter. Bengaluru and Hyderabad emerged as frontrunners for demand of Grade A office space in Q1 2024, cumulatively accounting for more than half of the India leasing activity. Overall office demand across the top six cities also remained robust, at 13.6 million sq ft, marking a remarkable 35 percent increase compared to the same period last year.

Following a remarkable surge in investments in industrial and warehousing assets in 2023, the segment maintained its momentum, capturing an 18 percent share of total inflows in Q1 2024. A steady investment inflow of USD 0.2 billion during the quarter, similar to the same period previous year, indicated sustained growth in the particular segment. As the segment evolves, and micro-fulfillment centers, dark stores and AI-driven supply chain becomes more prevalent, consolidation and instutionalization will pick up pace, further driving global capital in the coming years.

Investment Inflows (USD Million)

*Note: Alternate assets include data centers, life sciences, senior housing, holiday homes, student housing, schools, etc.

Source: Colliers

“With IMF’s projected GDP growth rate of 5.7 percent in 2024, India continues to garner significant investor interest within the APAC region. In Q1 2024, the APAC region contributed to over 82 percent of foreign inflows in India’s real estate sector, with investments predominantly focused on office assets followed by industrial & warehousing segment. The surge in investments by APAC countries such as Singapore can be attributed to a combination of factors including favorable investment climate, strong demand fundamentals across core & non-core segments within real estate, and strategic alliances in the form joint venture platforms. Amid evolving global capital trends, India’s real estate market promises significant growth potential and will continue to attract global capital from diverse regions,” said Vimal Nadar, Senior Director and Head of Research, Colliers India.

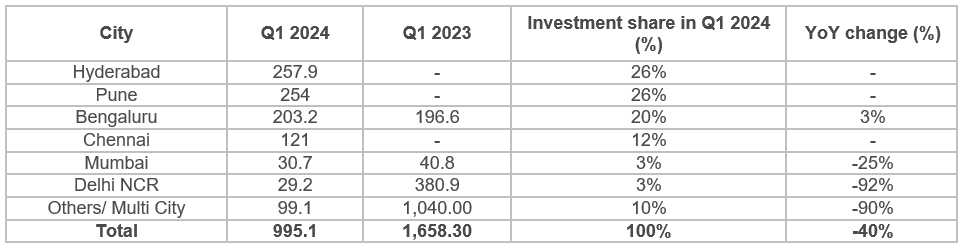

In Q1 2024, Hyderabad and Pune collectively attracted over 50% of the investment inflows in India, notably drawing substantial capital into office spaces and industrial & warehousing assets. These cities, alongside Bengaluru, solidified their positions as prime destinations for office sector investments. At the same time, investments in Industrial and warehousing assets were concentrated in Pune, Chennai, and Delhi-NCR, indicating robust industrial activity in these cities.

City-wise investment Inflows in Q1 2024

Source: Colliers

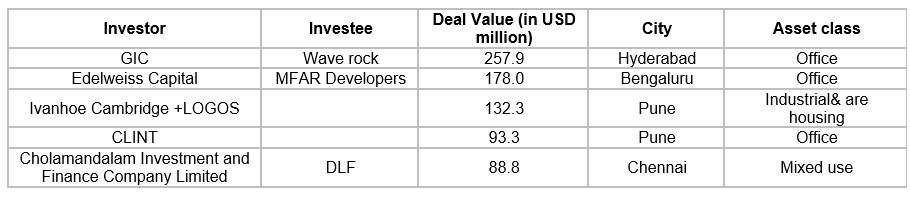

Top 5 deals in Q1 2024

Source: Colliers

Hyderabad and Pune collectivelly attracted over 50 percent of the investment inflows, notably drawing substantial capital into office spaces and industrial warehousing assets. These cities alongside Bengaluru fortified their positions as prime destinations for office sector investments. Pune, Chennai, and Delhi-NCR have emerged as select cities where investments in industrial and warehousing assets are concentrated.

1

2

3

4

5

6