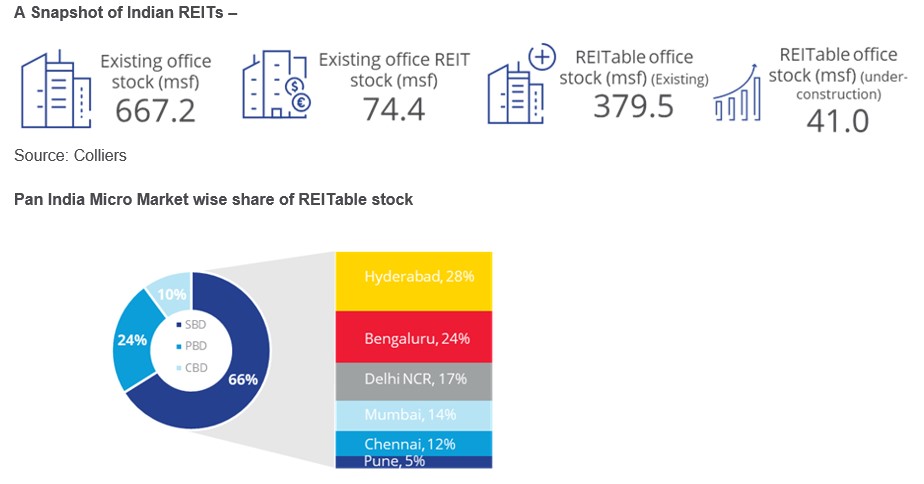

Holding about two-third of the overall REITable office stock in the top six cities of Mumbai, Delhi-NCR, Bengaluru, Chennai, Pune and Hyderabad, Secondary Business Districts (SBDs) hold great promise for the growth of Grade A REITable office space in India

Amongst the SBDs of the top six cities , the SBD of Hyderabad holds the highest quantum of REIT-worthy stock with 28% share, followed by Bengaluru at 24%. Further, over 60% of the Grade A stock within SBDs is REIT-worthy. At the same time, about half of the total Grade A office stock in Peripheral Business Districts (PBDs) across the top six cities is REIT-worthy. Understandably, the Central Business Districts (CBDs) have a relatively lower share of REITable stock, at 10%, due to limited new supply and presence of relatively older buildings.

According to Colliers’ recent report on ‘REITs- gaining larger ground in Indian Real Estate’, REITs have gained significant market as a promising alternate real estate platform and hold a huge potential to attract investments into the real estate sector.

A Snapshot of Indian REITs –

Source: Colliers

Pan India Micro Market wise share of REITable stock

Note: CBD – Central Business District; SBD – Secondary Business District; PBD – Peripheral Business District

SBDs of the top six cities include- Bengaluru- SBD 1, SBD 2, ORR; Chennai- Guindy, OMR Pre-toll, MPR, PTR; Delhi NCR- Southern Peripheral Road (SPR), Techzone Greater Noida, Udyog Vihar, Hyderabad- SBD, Off SBD; Mumbai- Andheri East, Worli/Prabhadevi, Lower Parel, Kalina, Powai; Pune- Baner, Balewadi, Bavdhan, Pashan, Hadapsar

At present, the three listed office REITs cumulatively hold approximately 74.4 mn sq ft of office REIT stock, representing around 11% of the total existing Grade A office stock.

The underlying office sector has demonstrated resilience, particularly in the top six cities, with strong occupancy levels, despite looming externalities affecting demand. Office vacancy levels remained stable in Q1 2023 at 16.4%, pointing to a fundamentally strong commercial office market. The outlook for the office sector remains optimistic led by technology & flex space, with market likely to bounce back in the latter part of the year.

“REITs in India are still at their early stages compared to other regional markets. Strikingly, the market capitalization of Indian REITs is <10% compared to the USA, Singapore, and other countries in the APAC. Considering the size of the Indian office market there exists a huge potential for more number REITs and expansion of current REITs. The overall returns on listed REITs in India, including dividend yield, have been a major factor in the success of REITs in the country. The regulatory structure has also evolved and fallen in line with global best practices. In years to come, we are likely to see REITs expand to other asset classes such as Industrial, Data Center, Hospitality, Healthcare, and Education,” says Piyush Gupta, Managing Director, Capital Markets and Investment Services, Colliers India.

Huge Untapped REITs Potential

About 380 mn sq ft of the existing Grade A office space qualifies to be listed as REITs , but 57% of this stock remains untapped . Amongst the top six cities, Bengaluru leads with the largest share of REITable stock at 25%, followed by Hyderabad at 19%. Furthermore, an additional 41 mn sq ft of under-construction office stock, which is expected to enter the office market by the end of 2023, holds the potential to be REITed.

The three office REITs in India have been able to establish a strong platform to evince amongst global investors’ interest to commit funds in development-based assets. REITs are evolving and have paved the way for other asset classes as well. India’s first Retail REIT was listed on stock exchange in May 2023, expanding the investible cosmos for investors.

Low Market Capitalization Holds Great Potential For Growth

India is still a relatively smaller market compared to its counterparts in APAC, Europe & America and this can be gauged from a comparison of the market capitalization of the listed REITs. India’s REIT market capitalization accounts for less than 10% of the market capitalization of other countries like the USA and Singapore. However, India’s REIT market is poised for higher growth and has significant potential. With an existing REIT penetration rate of 11%, India has significant room to increase its REITable share up to 68%, aligning with other APAC countries like Singapore and Japan which have more than 50% of their office portfolio under REITs. A larger share of REITs in office portfolio can lead to the corporatization of the office sector and enhance credibility for investors led by the stringent regulatory requirements for REITs.

“India’s office sector continues to remain upbeat despite global business slowdown. The strong underlying demand for office sector paired with relatively lower costs of quality assets & improving regulatory environment has created a conducive ecosystem for the growth of REITs in India. Albeit at a nascent stage, REITs already account for an impressive 11% of the overall Grade A office stock in the country with an additional unrealized potential of 57%, equating to about 380 mn sq ft of incremental REITable office space. Led by new-age quality assets with higher occupancy levels. quality supply in pipeline and sturdy demand, SBDs are likely to see a higher proportion of REITable stock in the next few years,” according to Vimal Nadar, Senior Director & Head of Research, Colliers India.

Post the maiden retail REIT, the market is ripe to see the listing of REITs in industrial & warehousing sector while it continues to gain larger ground in existing asset classes. As real estate continues to get regulated with best practices, unitization of assets will only aid in boosting investor confidence, enhancing trading & liquidity for a market price discovery while corporatizing real estate at large.

1

2

3

4

5

6