The record growth of flex space, together with Global Capability Centres has contributed significantly to the highest quarterly office space transaction volumes over the last two years, in turn leading to fall in space vacancy across markets during the first half of 2023.

According to Knight Frank India H1 2023 report, the office market saw robust activities during the first half of the year on the back of the undercurrent of economic stability. The growth is also reflected in the relatively stable occupier activity. The office space demand was resilient with 26.1 mn sq ft of transacted space- a 3% YoY growth in terms of volume. In fact, the momentum seemed to be increasing toward the end of the period as 14.8 mn sq ft space was transacted in Q2 2023, the highest quarterly tally since Q1 2021. Office space vacancy has reduced in most markets amidst demand for flex spaces reaching a record high.

Transaction volumes which have ranged within a tight band of 25-26 mn sq ft over the past four half-yearly periods showcase the resilience of the Indian office market in the backdrop of a turbulent economic and geopolitical environment across the globe. Additionally, the Indian office market was not as impaired by the remote working phenomenon as the rest of the world, due to the greater influence that employers have in India and their willingness to adopt flexible working options to address contemporary concerns.

Transaction volumes in Chennai and NCR grew the most at 104% and 24% YoY respectively during the period. Bengaluru with 7.0 mn sq ft, constituted 27% of the area transacted. NCR with 5.1 mn sq ft, is a distant second whereas Chennai and Mumbai with 4.5 mn sq ft and 3.2 mn sq ft took the third and fourth spot respectively.

Market Summary: Top Eight Indian Cities

Source: Knight Frank India

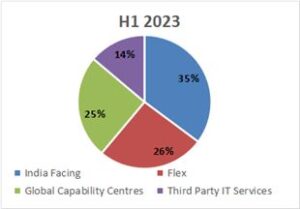

India-facing businesses have been gaining traction in recent times as growth capital is increasingly finding its way into the country, due to the relatively favourable economic environment here. This has been reflected in the increasing volume of office space taken up by such businesses which have amounted to 35%, Flex spaces accounted for 26%, global capability centres at 25%, and third-party IT services at 14% of the total volume transacted in H1 2023. Third party IT services have come down largely due to hybrid and budget cuts by the clients. Other service sector companies such as those from the healthcare, education, and e-commerce segments constituted approximately 49% of these India-facing businesses while BFSI and manufacturing companies accounted for 28% and 13% of the same.

The demand for flex spaces which has been rising consistently over the past few years has only received an added boost by the pandemic. The share of flex spaces has scaled a new high of 26% in H1 2023 and depicts the accelerated growth vector that this segment has firmly embarked on.

End-use Split of Transactions in H1 2023

Source: Knight Frank India

Source: Knight Frank India

Notes:

While office space demand has remained extremely resilient, the supply volumes have dropped approximately 25% YoY in H1 2023. The comparatively lower 18 mn sq ft delivered during the period has pulled down vacancy from 17% in H1 2022 to the 16.4% currently. The lower volume of office completions has thus helped the market maintain a healthy equilibrium in the backdrop of global headwinds that pose a challenge. Bengaluru and NCR accounted for 57% of the total space delivered during H1 2023.

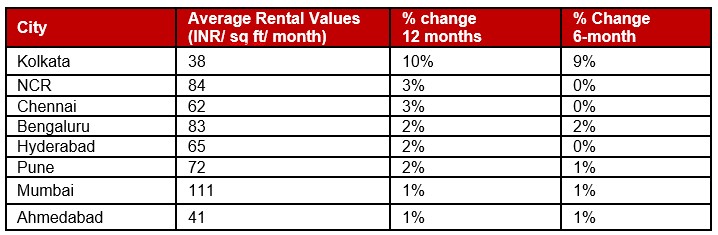

Rental values were stable or strengthened across all markets in H1 2023. While rents have grown in the range of 1% to 3% for most markets, rents in Kolkata have grown by 10% YoY due to very little supply coming up since the pandemic hit in H1 2020. The year 2023 has begun on a good note for the Indian office market, and the improving physical occupancy levels observed across the eight markets, also reported by REITs, are an encouraging indication for the year ahead.

Market Wise Rental Movement

Source: Knight Frank India

According to Shishir Baijal, Chairman and Managing Director, of Knight Frank India, India’s office market displayed remarkable resilience and the strengthening economic fundamentals provide a solid foundation for the office market especially to the growth of India facing businesses which are expected to sustain demand throughout 2023.

1

2

3

4

5

6